Brexit and Beyond 2 - the impact on cereals

21st October 2016 by Cedric Porter

This is the second in our special series, in which supply chain expert and former Oxford Farming Conference chairman Cedric Porter discusses the impact of Brexit on the cereal sector.

The immediate effects of Brexit were largely positive for the UK grain industry, with a plunging pound making the UK more competitive. But then the reality of the global market kicked in and even a poor European harvest did little to reduce the world’s stockpiles of grain and prices remained subdued.

In many ways Brexit is a sideshow for the cereal sector with the future of support perhaps the most pressing issue. Currently only a very few British growers will be making money without support and there will be concerns as to the future of payments after 2020. But Brexit will have little impact on the fundamentals of the grain market including the weather, demand and production in other parts of the world.

World cereal yields in t/ha ranked on wheat yields

| Wheat | Barley | Oilseed Rape | |

|---|---|---|---|

| New Zealand | 9.1 | 6.8 | 1.1 |

| Belgium | 8.9 | 8.3 | 4.3 |

| Ireland | 8.9 | 7.6 | 3.6 |

| Netherlands | 8.7 | 7.0 | 3.0 |

| UK | 8.6 | 6.4 | 3.6 |

| Germany | 8.0 | 6.6 | 3.9 |

| Denmark | 7.3 | 5.7 | 3.9 |

| France | 7.2 | 6.3 | 3.0 |

Source: Defra 2014 & UN FAOSTAT 2013 figures

The UK is a relatively major player on the global cereal market as a top 15 wheat producer. But it arguably punches above its weight because of its large population and its long history of developing new varieties and growing techniques. The UK is also very good at producing grain efficiently. It is a British farmer who currently holds the world wheat yield record and only a few other countries in the world can consistently deliver such high-yielding crops with most of those that can not significant world producers.

It is important that the UK grain industry makes the most of its natural advantages both before and after Brexit. Consumption of grain-based products may be static at best in the UK but a rising population does still mean there are plenty of opportunities. However, the buoyancy of the UK market will attract the attention of other countries, especially those in Europe where populations are declining such as Germany and even Russia.

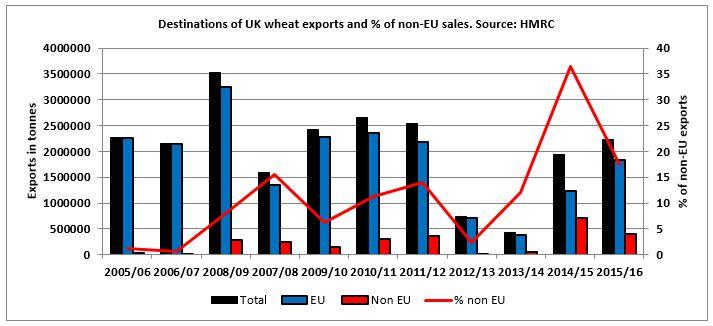

Cereals are one of the few commodities where the UK has an exportable surplus. There are already signs that UK shipments are shifting away from the EU to outside it, although the union is still the biggest market. In the 2015/16 season 17.5% of wheat exports were outside the EU and in 2014/15 it was 36.5% which compares to 11.4% over the last 11 seasons. Barley exports outside the EU account for a round a third of shipments every year with the proportion rising.

By focusing on what it does well, such as growing top quality biscuit wheat and malting barley that few other countries can, backed up with schemes such as AHDB’s uks and ukp export brands and assurance marques from the likes of Red Tractor, LEAF and the Soil Association, then Britain could continue to carve out high value niches for itself after Brexit.

• Northumberland farmer Rod Smith holds the world wheat yield record at 16.52 tonnes/hectare set in 2015¹

• UK wheat yields have quadrupled in the last 75 years²

• Rothamsted’s 20:20 Wheat programme aims to achieve 20 tonnes/hectare within 20 years³

• The world is short of the group 3 biscuit wheat the UK excels at growing ⁴

• World demand for malting barley is expected to grow by 14% in the next five years ⁵

• The UK cropped area is down 10% since 1985 ⁶

Sources:

¹ Farmers Weekly 21 September 2015, ² British Society of Plant Breeders, ³ Rothamsted, ⁴ FG Insight 22 July 2016, ⁵ Rabobank March 2016, ⁶ Defra